SEP IRA Contribution Limits For 2024 And 2025

The SEP IRA allows you to contribute up to 25% of your compensation, or $69,000 in 2024 and $70,000 in 2025.

Remember, you can contribute to your SEP IRA all the way up until the tax deadline – April 15.

Whether you’re a side hustler or a full-time entrepreneur, a SEP IRA or Simplified Employee Pension Individual Retirement Account, may allow you to boost investment returns by reducing your taxes while saving for retirement.

SEPs were created for small business owners with employees and those who are self-employed, without any employees. They’re a sort of like a mix between a 401(k) and traditional IRA.

Before you open an account, find out whether you’re eligible and how much the contribution limits are.

A SEP IRA is a retirement account designed specifically for the self-employed and people that own small businesses. Business owners can make contributions to SEP accounts for themselves and employees. Once the contributions are made, the account is owned completely by the employee. However, employees can’t make their own contributions to the plans.

Compared with traditional 401(k) plans, SEP IRAs are typically easier for you, the business owner, to create and maintain without a lot of accounting stress. Most brokerages allow you to open SEP accounts for yourself and your employees. You can make contributions by mailing in checks or through electronic transfers.

Anyone with self-employed or small business income may qualify to contribute to a SEP-IRA. If you have employees, you must contribute an equal portion of compensation for yourself and your employees. Most people working in the gig economy will qualify to open a SEP IRA since they earn 1099-NEC income.

In 2024, you can contribute 25% of your total compensation to an IRA with a maximum contribution of $69,000.

For self-employed people compensation is your revenue, less expenses including half of your self employed taxes. The example below shows how a self-employed person can figure out their maximum contribution.

|

Net Income (Revenue minus Expenses) |

|

|

Income, less self-employed taxes (Net Income minus half of self-employed taxes (Net Income x 7.65%) |

$150,000 – $11,475 = $138,525 |

|

Contribution Limit (25% of above) |

$138,525 x 0.25 = $34,631.25 |

If you have a workplace 401(k) and a SEP IRA, you can contribute to both of these accounts. In 2024, you can contribute $23,000 to a 401(k) and up to $69,000 to a SEP-IRA (depending on your earnings). If you have employees, you must contribute at the same rate for them as you do for yourself.

Remember, a SEP IRA is a traditional IRA. As such, you can make traditional IRA contributions to it as well as your employer. Employer contributions don’t contribute to your IRA contribution limit, but your contributions would.

Note: Be careful if you have a third retirement account, such as a Roth IRA. Funds that you contribute (not the employer) to a SEP IRA will reduce the amount you can contribute to your other IRAs.

You can typically choose between a traditional IRA, a Roth IRA and SEP IRA for retirement contributions. Each account has its own benefits and drawbacks. This chart compares some of the attributes for each account type.

Remember, though, that the SEP IRA requires you to have a business.

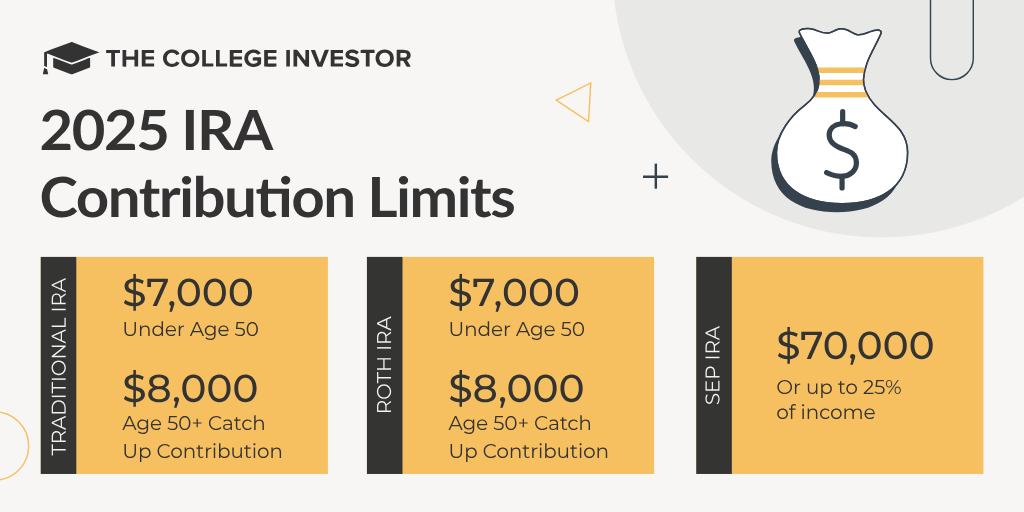

Here are the 2024 IRA Contribution Limits:

Source: The College Investor

In 2025, the limits for the SEP IRA will go up slightly:

Source: The College Investor

If you own a business, you’ll likely need to choose between a small business 401(k) and a SEP for their business. A SEP is entirely funded by employer contributions, whereas a 401(k) is funded by both employee and employer contributions.

If you have employees you may choose a SEP IRA for the contribution flexibility. Your contribution rate and your employees range from 0% up to 25% of total compensation.

There are restrictions you can choose to limit contributions. For example, you only contribute if your employees meet all three of the following criteria:

You can also choose to make contributions for yourself and employees per year instead of worrying about contributing with each paycheck, unlike a 401(k).

Setting up these accounts was one of the biggest issues we hear from readers, so we put this review together for you.

Contributions for yourself and your employees are due by the tax filing due date (including extensions). That means you must make a contribution by April 15 or October 15 if you filed an extension.

Investing in a retirement account offers tremendous tax advantages, but you may not want to lock your money away.

If you have major investments or expenses coming up, you may want to delay contributions until next year. But don’t wait too long to invest so you can take advantage of compounding growth as soon as possible.

The Best Online Stock Brokers—According to Readers

If you’re still stuck in choosing a SEP IRA, Solo 401(k), or SIMPLE IRA for your business, you can use any of these top online brokers to help you open an account. We polled our readers for this one!

The Securities and Exchange Commission (SEC)’s next Enforcement Division Director will be David Woodcock, a partner at Gibson Dunn &...

Only about 12% of college students pay full sticker price. The share paying the advertised rate has been shrinking for...

Publications Archives UnfavoriteFavorite April 7, 2026 Shared Success, and Economic Opportunities Program Tim Ogden Managing Director, Financial Access Initiative, NYU...