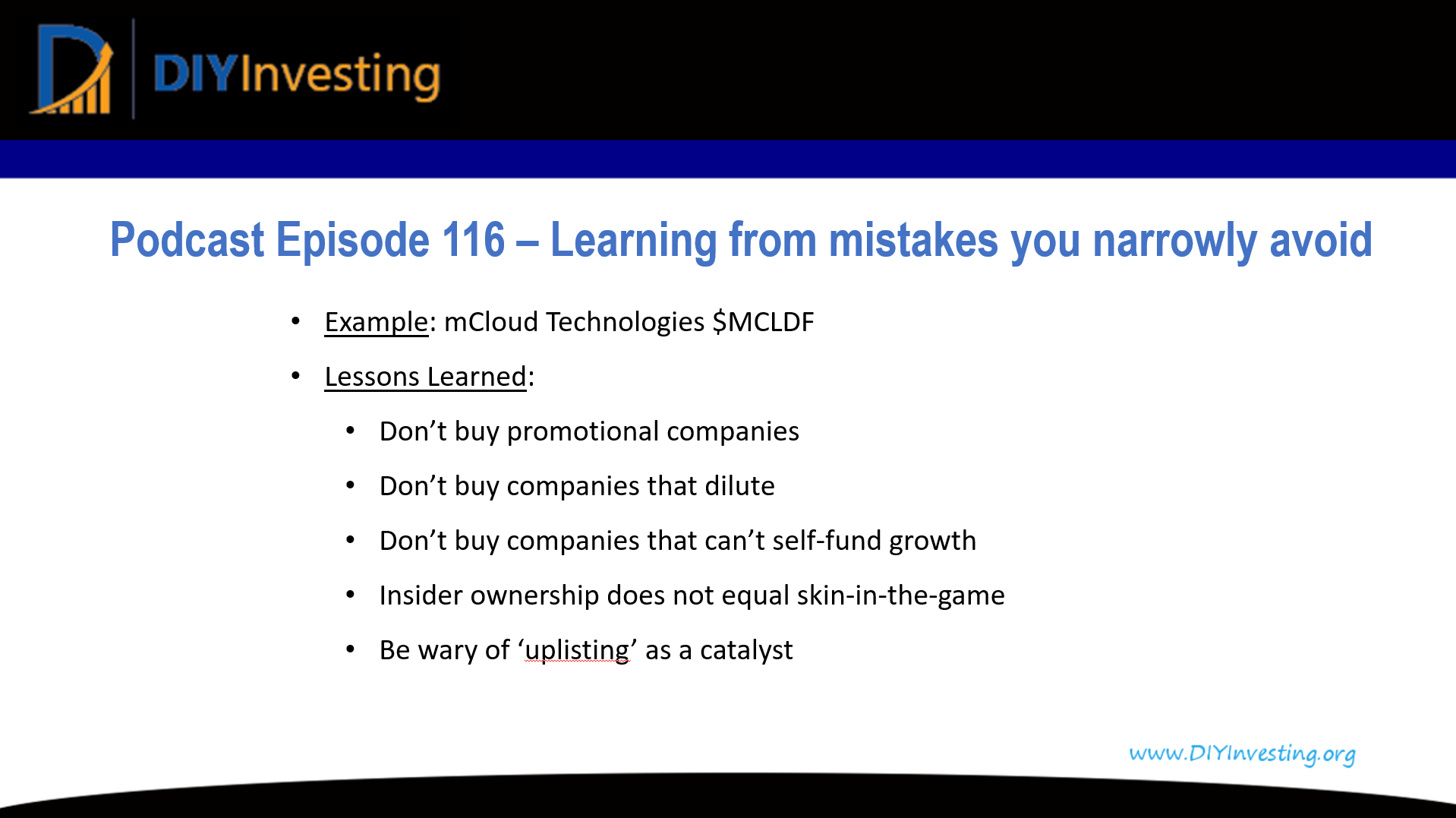

116 – Learning from mistakes you narrowly avoid $MCLDF

If you enjoyed this podcast and found it helpful, please consider leaving me a rating and review. Your feedback helps me to improve the podcast and grow the show’s audience.

Twitter Handle: @TreyHenninger

YouTube Channel: DIY Investing

This is a podcast supported by listeners like you. If you’d like to support this podcast and help me to continue creating great investing content, please consider becoming a Patron at DIYInvesting.org/Patron.

Investors need to constantly be wary of confirmation bias and stay alert for possible red flags. mCloud Technologies stock $MCLDF taught me this lesson. Don’t buy promotional companies that dilute shareholders and can’t self-fund growth.

Liked it? Take a second to support DIY Investing on Patreon!

A new House Judiciary Committee report finds that the National Resident Matching Program (NRMP), known as the Match, operates as...

In my journey toward financial independence, I’ve found one habit to be more important than all the others. This is...

Jun 17, 2026 TO Jun 18, 2026 | Chicago One location with everything you need to develop your practice. At...